Новини та аналітика

06.02.2026

Summary of 2025

The 2025 review provides an important context for assessing the market’s behavior under stress. Energoatom generated 53,730 thousand MWh (+1.2% y/y), with the main share contributed by the South Ukrainian, Khmelnytskyi and Rivne NPPs. The total trading volume on the spot market in 2025 reached 33.51 TWh — 22% more than a year earlier, indicating an increased role of spot instruments in ensuring short-term balances.

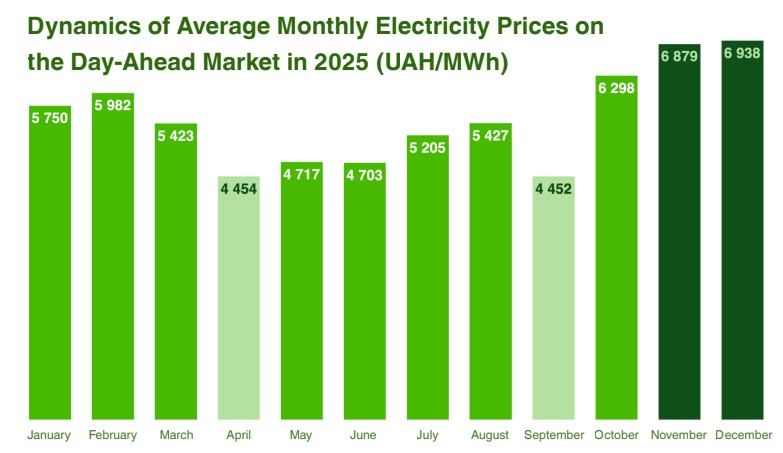

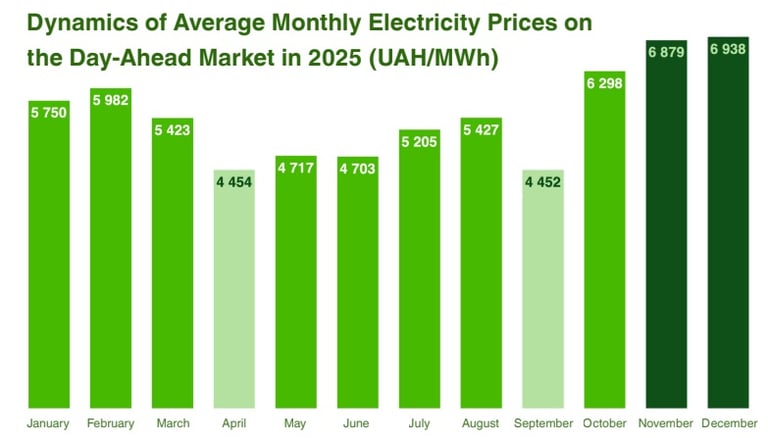

At the same time, the market demonstrates high seasonal and short-term volatility: the weighted average price of the RDN is UAH 5,643.94/MWh with a maximum at the end of the year (up to UAH 8,220.83/MWh) and a minimum in May (~ UAH 2,446/MWh); on the VDR, the amplitude is even wider - from ~2,183 UAH/MWh to peak ~10,804 UAH/MWh. Such dynamics indicate that even with an overall market surplus, short-term deficits during peak hours can create significant price shocks and increase operational risks for suppliers and consumers.

Under Pressure: Ukraine's Energy Sustainability — Market Overview for January 2026

January 2026 revealed the high vulnerability of Ukraine’s power system due to massive attacks and extreme weather conditions, which caused an emergency mode, emergency outages and local shortages (up to ~500 MW in Kyiv, ~30% nationwide during critical hours). Accelerating the development of cogeneration, distributed generation and coordinating policies and financing are key to increasing resilience in the short and medium term.

Air attacks and the operational state of Ukraine’s power system

January 2026 was a serious test for Ukraine’s power system: massive attacks on infrastructure, coupled with severe weather conditions, put the system into an emergency mode.

wrote by Daria Karpuk for UKRTEPLO

Outages and capacity restrictions have affected large cities — primarily Kyiv and Kharkiv — as well as southern and eastern regions; the capital has an estimated electricity deficit of around 500 MW, and around 30% nationwide during peak hours. This means that technical reserves and local capacity to meet demand are not keeping up with rapidly changing load parameters and supply chain disruptions.

In January 2026, all 9 NPP units were operating on the grid, providing baseload generation, while coal reserves (~2.2 million tons) provided headroom for peak loads. However, nuclear units have proven vulnerable to short-term power outages during attacks, and fuel reserves are only useful if logistics are stable. In response to these challenges, imports from the EU (up to ~2 GW during the evening peak) and an increase in the capacity of the crossings with Moldova to 2,450 MW have become critical balancing tools.

Structural shifts in generation and financing

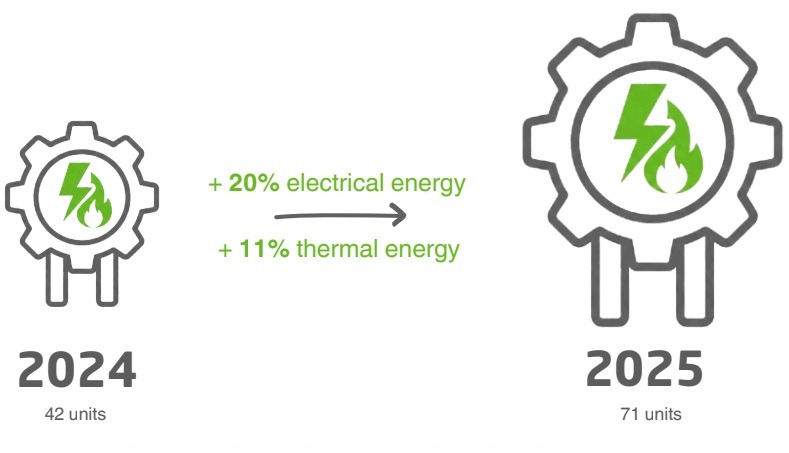

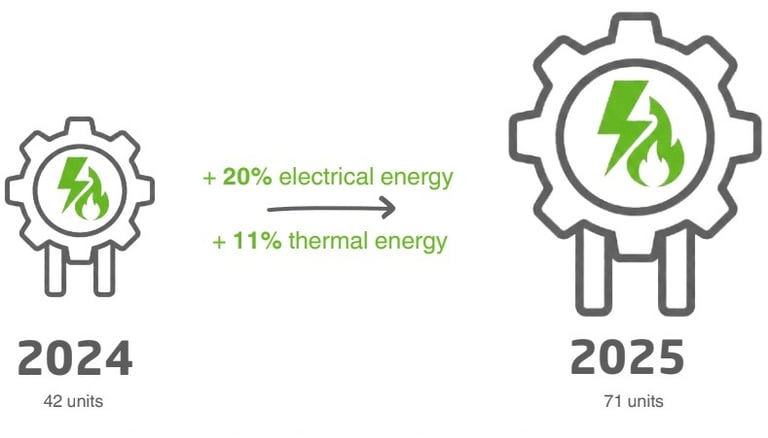

In parallel with the increase in price volatility, a visible structural transformation of the generation landscape is taking place. In 2025, the State Energy Efficiency Agency qualified 71 cogeneration plants (versus 42 in 2024), the total installed capacity of such facilities reached ~3.1 GW of electricity and 9.2 Gcal/h of heat. Regional plans provide for the installation of at least 250 new cogeneration plants (~1.1 GW) over the next two years. About 762 MW of new distributed generation has also been introduced - mainly small solar systems (5–30 kW) under the “green” tariff and interest-free loan programs.

Financial support is accelerating these developments: the government has allocated UAH 2.56 billion from the reserve fund for mobile distributed generation, while support packages for SMEs are in place (there are one-time payments for individual entrepreneurs and loans under the “5-7-9%” program for the purchase of generators and batteries). From June 2024 to January 2026, banks financed projects worth UAH 35.3 billion in 21 regions, directing capital mainly to generation (1.342 GW) and storage (543 MW). These financial flows lower the barriers to entry, but the speed of project implementation and coordination of actions remain key.

Risks and policies

The short-term vulnerability of the system is determined by operational risks due to attacks, logistical problems with fuel supply, and network “bottlenecks” that turn the overall surplus into momentary deficits. Medium-term risks are related to finance - a slowdown in lending or an increase in the cost of capital may slow down energy projects.

In practice, this means: the regulator must urgently simplify the connection of distributed generation and create effective financing mechanisms; operators - invest in load shedding automation and local reserves to minimize socio-economic losses from outages; businesses - diversify energy sources (a combination of generators, batteries, long-term import contracts); investors - focus on cogeneration and distributed energy solutions with state/bank support.

January 2026 confirmed: the transformation from centralized vulnerability to distributed resilience is underway, but the pace and coordination of actions will determine whether the system will survive the next winter peak without large-scale economic losses. Politics, financing, and technical modernization must operate in synchrony—otherwise, every massive attack by an aggressor will become a serious test of endurance.